Usually salary income is chargeable to tax either on due basis or on receipt basis. For the purpose of changeability salary consist of;

- Any salary due from an employer including former employer in the previous year, whether or not actually received.

- Any salary paid or allowed in the previous year by or on behalf of employer including former employer, although not due or before it became due, and

- Any arrears of salary paid or allowed in the previous year by or on behalf of employer including former employer, if not charged to income tax in any of the previous year.

If an employee is in receipt of any component of his salary in arrears or paid in advance, or receives profit in lieu of salary, he can claim relief as allowed by Section 89 read with rule 21A of Income Tax Act and Income Tax Rules. The relief can be claimed for following;

- Relief in respect of salary or family pension received in arrears or in advance [Rule 21A(2)]

- Relief in respect of gratuity [Rule 21A(3)]

- Relief in respect of compensation on termination of employment [Rule 21A(4)]

- Relief in respect of payment of commutation of pension [Rule 21A(5)]

- Relief in respect of other payment [Rule 21A96)]

Provided that no such relief shall be granted in respect of any amount received or receivable by an assessee on his voluntary retirement or termination of his service, in accordance with any scheme or schemes of voluntary retirement or in the case of a public sector company, if an exemption in respect of any amount received or receivable on such voluntary retirement or termination of his service or voluntary separation has been claimed by the assessee under clause (10C) of section 10 in respect of such, or any other, assessment year.

Click here to Download Automatic Arrears Relief Calculator with Form 10E from F.Y. 2000-01 to F.Y. 2017-18 (Up to date Version) in Excel.

Now let us elaborate and understand the each case separately.

Relief in respect of salary or family pension received in arrears or in advance [Rule 21A(2)]

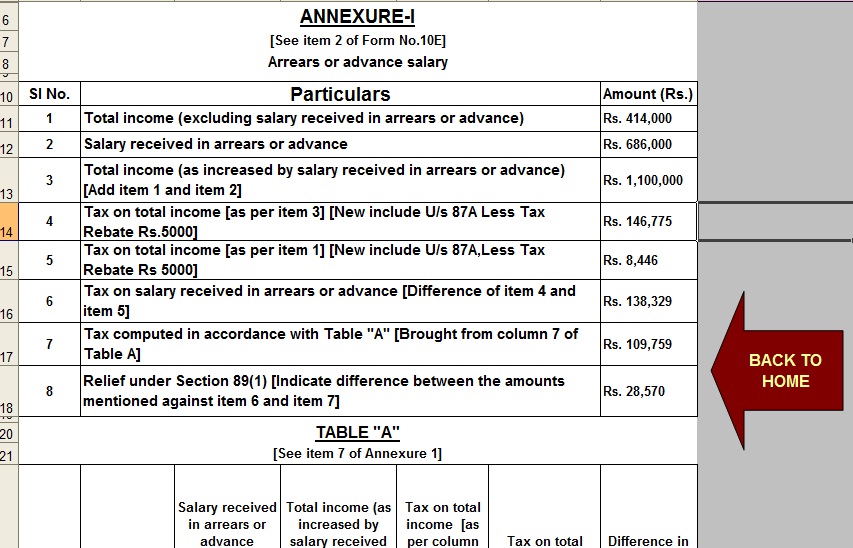

The relief on salary received in arrears or in advance is computed in the manner as refined by rule 21A(2) which is produced as below;

- Calculate the tax payable on the total income, including the salary received in arrears or in advance, of the relevant previous year in which the same is received.

- Calculate the tax payable on the total income, excluding the salary received in arrears or in advance, of the relevant previous year in which the additional salary is received.

- Find out the difference between tax at (1) and (2).

- Compute the tax on the total income after including the salary received in arrears or in advance in the previous year to which such salary relates.

- Compute the tax on the total income after excluding the additional salary in the previous year to which such salary relates.

- Find out the difference between tax at (4) and (5).

- Amount of relief: The excess of tax computed at (3) over tax computed at (6)

Relief in respect of gratuity [Rule 21A(3)]

Relief for gratuity can is claimed if the amount of gratuity received is in excess of gratuity specified under section 10(10). However no relief is permissible if the taxable gratuity is received for less than 5 years of service period. The amount of relief is admissible in the as per following category

- Where gratuity payable is in respect of past service of 15 years or more

The amount of relief is calculated as follows:

- Compute the average rate of tax on the total income including the gratuity in the year of receipt

- Find out the tax on gratuity at the average tax rate as computed in (1)

- Compute the average rate of tax by adding 1/3 gratuity to preceding 3 previous years

- Find out the average of 3 years average rate as computer in (3) and compute the tax on gratuity at that rate

- Relief admissible : difference between (2) and (4)

2. Where such period is 5 years or more but less than 15 Years

The amount of relief for this category , the relief is calculated as on the similar lines of above with only difference that instead of average of average rates of 3 years, the average of average rate of 2 years shall be taken by adding ½ of gratuity to each of two preceding year.

Relief in respect of compensation on termination of employment [Rule 21A(4)]

If the compensation received by the employee from his current or previous employer at or in relation with termination of his employment after completion of 3 years of service and unexpired portion of his term of employment is more than 3 years, the relief is calculated in the same manner as if gratuity paid to employee in respect of service rendered for a period of 15 years or more.

Relief in respect of payment of commutation of pension [Rule 21A(5)]

A relief can be claimed in respect of commutation of pension received in excess of limits specified under section 17(1)(ii). Such relief is computed in the same manner as if gratuity paid to employee in respect of service rendered for a period of 15 years or more.

Relief in respect of other payment [Rule 21A(6)]

In respect of any other payment received by employee other than those specified above, the relief will be granted by the CBDT after examination of circumstances of each case.

Procedure for claiming the tax relief – In order to claim tax relief under the aforesaid circumstances, the employee should give relevant information in his income tax return.

Basically relief under section 89 is arithmetical. It involves finding out two tax rates.

Read with Rule 21A, With Automatic Arrears Relief Calculator with Form 10E U/s 89(1)){kind=link}

0 Comments